What Is Risk Management? A Complete Guide for Businesses

Published: June 5, 2026

Last Updated: June 5, 2026

A ransomware attack shuts down operations. A supplier unexpectedly goes bankrupt. A new regulation creates compliance obligations across multiple business units. In many cases, the biggest challenge is not the event itself, but the fact that the organization was not prepared for it.

The most resilient organizations do not rely on luck when navigating uncertainty. They use structured risk management practices to identify potential threats, evaluate their impact, and determine the best course of action before problems escalate. The objective is not to eliminate every risk, but to make informed decisions that protect business objectives while supporting growth.

Today, risk management extends far beyond insurance policies and compliance checklists. Organizations must manage a growing range of risks, including cybersecurity threats, operational disruptions, financial volatility, regulatory change, supply chain dependencies, and emerging technologies such as AI. As these risks become more interconnected, a proactive and organization-wide approach becomes increasingly important.

In this guide, we’ll explain what risk management is, explore the most common types of business risk, break down the risk management process, examine proven risk response strategies, and show how organizations can build a practical risk management program that strengthens resilience and supports long-term business success.

Key Takeaways

- Risk management helps organizations identify, assess, and respond to risks before they affect business objectives.

- The most common business risks include financial, operational, cybersecurity, strategic, compliance, reputational, and ESG-related risks.

- An effective risk management process follows 5 steps: identify, assess, prioritize, respond to, and continuously monitor risks.

- Organizations can manage risk through 5 response strategies: avoid, reduce, share, transfer, or accept the risk.

- In 2026, risk management is becoming more proactive, with continuous monitoring, stronger leadership accountability, and a greater focus on organizational resilience.

What Is Risk Management?

Risk management is the process of identifying, assessing, and responding to events that could affect an organization’s objectives. These events may create financial losses, operational disruptions, legal issues, cybersecurity incidents, or other challenges that impact business performance.

Organizations face risks from many sources, including market changes, human error, technology failures, regulatory requirements, supply chain disruptions, and natural disasters. Risk management helps businesses understand these uncertainties, evaluate their potential impact, and take appropriate action before they become larger problems.

Importantly, risk management is not only about preventing negative outcomes. It also helps organizations identify opportunities, make better decisions, and pursue growth with a clearer understanding of potential risks and rewards.

Types of Risk in Business

Every organization faces risk, but not all risks have the same source or impact. Some affect financial performance, while others can disrupt operations, create compliance challenges, or damage customer trust. Understanding these categories helps organizations assess risks more effectively and develop appropriate response strategies.

Below are 7 types of risk in business:

1. Financial Risk

Financial risk refers to anything that could negatively affect an organization’s financial performance. It occurs when external market conditions or financial events make it harder for a business to generate revenue, control costs, maintain cash flow, or meet financial obligations.

Example: A company that sells products internationally may see profits decline when unfavorable exchange rate movements reduce the value of overseas revenue.

2. Operational Risk

Operational risk arises when people, processes, systems, or suppliers fail to perform as expected. Because these activities support day-to-day business operations, even a small disruption can affect productivity, customer service, or business continuity.

Example: A critical supplier experiences a production outage, delaying deliveries and preventing the company from meeting customer orders on time.

3. Cybersecurity Risk

Cybersecurity risk involves threats that could compromise an organization’s systems, applications, networks, or data. As businesses become more dependent on technology, cyber incidents can disrupt operations, expose sensitive information, and create significant financial and legal consequences.

Example: A ransomware attack encrypts company data and prevents employees from accessing critical business systems until recovery efforts are completed.

4. Strategic Risk

Strategic risk occurs when business decisions, market conditions, or industry changes prevent an organization from achieving its long-term objectives. These risks are often linked to growth initiatives, competitive pressures, changing customer behavior, or emerging technologies.

Example: A company invests heavily in a new product line, but customer demand fails to meet expectations, resulting in lower-than-expected returns.

5. Compliance Risk

Compliance risk arises when an organization fails to meet legal, regulatory, contractual, or industry requirements. Changes in regulations, inadequate controls, or poor oversight can expose the business to penalties, legal action, or operational restrictions.

Example: A company fails to implement required data privacy controls and receives regulatory fines following an audit.

6. Reputational Risk

Reputational risk is the possibility of losing the trust and confidence of customers, investors, employees, or the public. While reputational damage often begins with another type of incident, the impact can last much longer and affect future business performance.

Example: Negative media coverage following a product safety issue causes customers to switch to competing brands.

7. ESG & Climate Risk

ESG and climate risk refer to environmental, social, and governance issues that can affect an organization’s operations, reputation, compliance obligations, or access to investment. As regulators and stakeholders increase their expectations, these risks are becoming a larger part of business decision-making.

Example: Severe flooding damages manufacturing facilities and disrupts supply chains, causing production delays and increased operating costs.

The Risk Management Process: 5 Key Steps

Risk management is not a one-time exercise. As business priorities, technologies, regulations, and market conditions change, organizations must continuously identify and address new risks. A structured process helps ensure risks are evaluated consistently and managed effectively over time.

Most risk management programs follow 5 core steps.

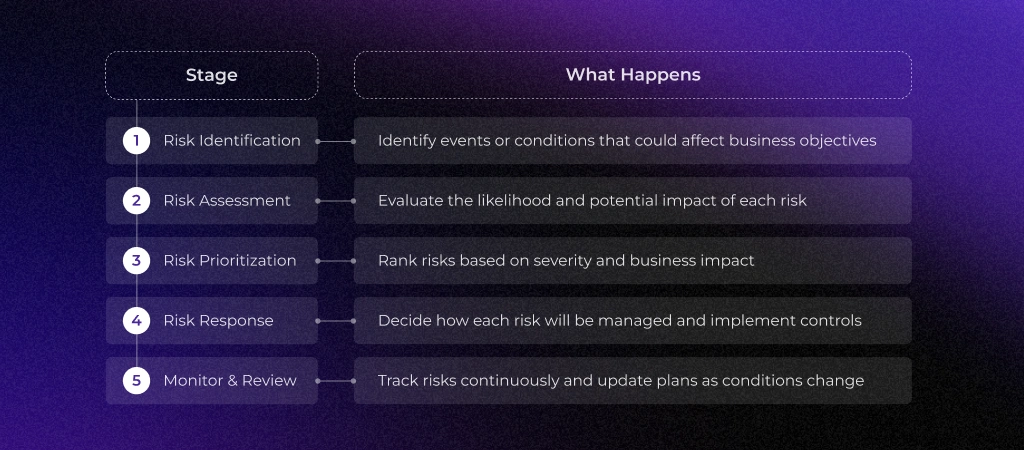

1. Risk Identification

The first step is identifying anything that could prevent the organization from achieving its objectives. Risks may come from internal operations, technology systems, employees, suppliers, regulatory changes, market conditions, or external events.

Many organizations document identified risks in a risk register, which serves as a central repository for tracking risks, ownership, mitigation plans, and status updates.

2. Risk Assessment

After risks have been identified, organizations evaluate how likely each risk is to occur and the potential impact it could have on the business. The purpose is to understand which risks pose the greatest threat to organizational objectives.

Risk assessments can be qualitative, using ratings such as low, medium, and high, or quantitative, using financial models and data analysis to estimate potential losses.

3. Risk Prioritization

Not all risks require the same level of attention. Risk prioritization helps organizations focus resources on the risks that could have the greatest business impact.

Many organizations use risk matrices, heat maps, or scoring models to compare risks and determine which issues should be addressed first.

4. Risk Response

Once risks have been prioritized, organizations decide how they will manage them. The objective is to reduce risk to an acceptable level while balancing business goals, available resources, and operational requirements.

Common response strategies include avoiding the risk, reducing its likelihood or impact, transferring it to a third party, or accepting it when the potential consequences fall within the organization’s risk tolerance.

5. Monitor & Review

Risk management is an ongoing process. New threats emerge, business operations change, and previously identified risks may increase or decrease over time.

Regular monitoring and review help organizations keep risk information current, evaluate the effectiveness of controls, identify emerging threats, and ensure leadership maintains visibility into the organization’s risk exposure.

Risk Management Strategies: The 5 Response Options

Identifying and assessing risks is only part of the risk management process. Organizations must also decide how they will respond to each risk based on its likelihood, potential impact, and alignment with business objectives.

While specific approaches vary by industry and situation, most risk management plans rely on 5 common responses.

1. Risk Avoidance

Risk avoidance means eliminating the activity that creates the risk altogether. Organizations choose this approach when the potential consequences outweigh the expected benefits or when the risk falls outside their acceptable risk tolerance.

By avoiding the activity entirely, the organization removes the possibility of the risk occurring. However, this may also mean giving up potential opportunities, revenue, or business growth.

2. Risk Reduction

Risk reduction aims to decrease either the likelihood of a risk occurring or the severity of its impact. Rather than eliminating the risk completely, organizations implement controls, processes, or safeguards that make the risk more manageable.

This is one of the most common risk management strategies because many business risks cannot be fully avoided but can be significantly reduced through planning, monitoring, and preventive measures.

3. Risk Sharing

Risk sharing involves distributing the potential impact of a risk across multiple parties. By sharing responsibility, organizations reduce the burden that a single entity would face if the risk materialized.

This approach is commonly used in partnerships, joint ventures, and collaborative business arrangements where both the benefits and risks are shared among participants.

4. Risk Transfer

Risk transfer shifts the financial or operational consequences of a risk to another party through a contractual arrangement. The risk itself does not disappear, but responsibility for managing certain consequences is transferred.

Organizations often use insurance policies, outsourcing agreements, warranties, or third-party service contracts as mechanisms for transferring risk.

5. Risk Acceptance

Risk acceptance occurs when an organization decides that the potential impact of a risk is within its risk tolerance and does not require additional action. This decision is typically made after evaluating the cost of mitigation against the potential consequences of the risk.

Accepting a risk does not mean ignoring it. Organizations continue to monitor accepted risks and prepare contingency plans where appropriate to ensure they can respond effectively if circumstances change.

Benefits of Effective Risk Management

Risk management is often associated with preventing problems, but its value extends far beyond risk reduction. A well-designed risk management program helps organizations make better decisions, strengthen resilience, and operate with greater confidence in an increasingly uncertain business environment.

When risk management becomes part of everyday decision-making, organizations are better positioned to balance growth opportunities with potential risks while maintaining operational stability.

1. Better Decision-Making

Risk management provides leaders with a clearer understanding of potential threats, opportunities, and business impacts before important decisions are made. This allows organizations to evaluate options more effectively and make informed choices based on both risk and reward.

2. Improved Business Resilience

Unexpected events such as cyberattacks, supply chain disruptions, regulatory changes, or economic downturns can significantly affect business operations. Risk management helps organizations prepare for these situations in advance and respond more effectively when disruptions occur.

3. Stronger Regulatory Compliance

Many industries operate under strict legal and regulatory requirements. Risk management helps organizations identify compliance obligations, monitor potential gaps, and implement controls that reduce the likelihood of violations, penalties, and audit findings.

4. Reduced Financial Losses

By identifying potential risks early and implementing appropriate controls, organizations can reduce the financial impact of incidents before they escalate. This includes avoiding unnecessary costs, minimizing operational disruptions, and protecting revenue-generating activities.

5. Increased Stakeholder Confidence

Customers, investors, partners, regulators, and employees expect organizations to manage risks responsibly. Demonstrating a structured approach to risk management helps build trust, strengthen credibility, and support long-term business relationships.

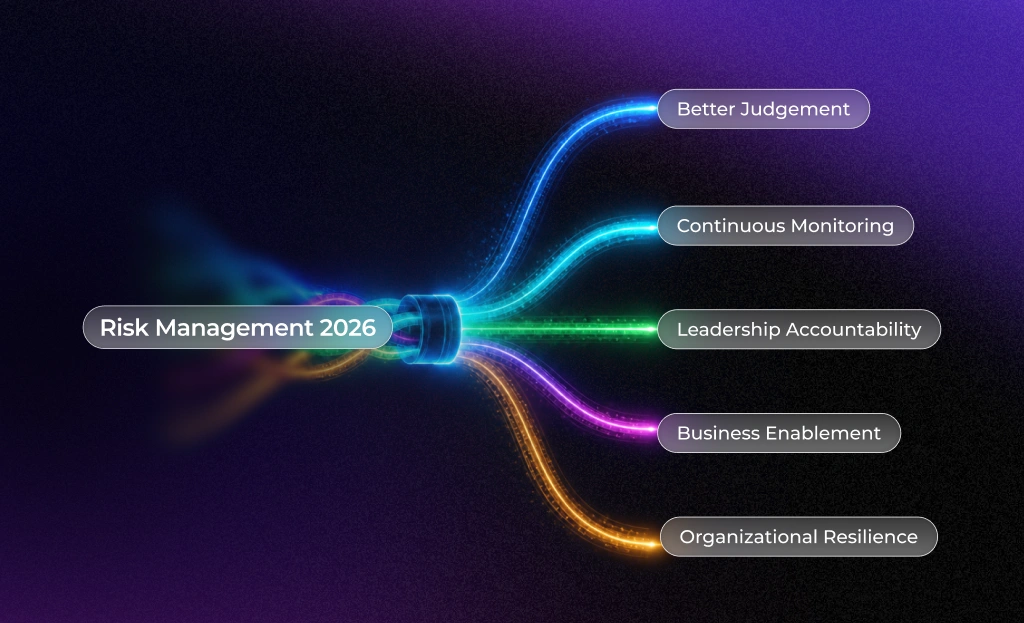

How Risk Management Is Changing in 2026

Risk management is no longer a process focused solely on compliance, annual assessments, and reporting. Organizations are operating in an environment where cyber threats evolve rapidly, regulations change frequently, and business decisions must often be made before complete information is available.

As a result, modern risk management is becoming more proactive, continuous, and closely integrated with business strategy. The following trends are reshaping how organizations identify, assess, and respond to risk in 2026.

1. From Checklists to Better Judgement

Traditional risk management frameworks often rely on policies, controls, and compliance checklists to guide decision-making. While these remain important, many modern risks involve complex situations that cannot be addressed through predefined rules alone.

Organizations increasingly need leaders and risk teams to apply judgement when evaluating uncertainty, balancing competing priorities, and making decisions in situations where there is no clear answer. Strong governance helps ensure these decisions are documented, consistent, and aligned with business objectives.

2. From Periodic Reviews to Continuous Monitoring

Annual risk assessments and quarterly reviews are no longer enough for many organizations. Cybersecurity threats, supply chain disruptions, regulatory updates, and market changes can emerge much faster than traditional review cycles.

To improve visibility, organizations are adopting continuous monitoring practices that provide ongoing insight into risk exposure, control effectiveness, and emerging threats. This allows issues to be identified and addressed before they develop into larger business problems.

3. Greater Accountability for Leadership

Risk management is becoming a leadership responsibility rather than a function managed solely by risk or compliance teams. Boards and executives are expected to understand key risks, evaluate trade-offs, and actively participate in risk-related decisions.

This shift reflects growing expectations from regulators, investors, customers, and stakeholders who want greater transparency and stronger accountability throughout the organization.

4. Risk Management as a Business Enabler

Organizations increasingly recognize that effective risk management does more than reduce losses and support compliance. It also helps leaders make better decisions, improve operational efficiency, and pursue growth opportunities with greater confidence.

When risk management is integrated into planning and decision-making, it can become a source of competitive advantage rather than simply a control function.

5. Building Resilience Instead of Predicting Everything

The pace of technological change, economic uncertainty, geopolitical events, and emerging threats makes it impossible to predict every potential risk. Rather than focusing exclusively on forecasting, organizations are investing more heavily in resilience.

This includes developing adaptable processes, strengthening business continuity capabilities, improving scenario planning, and creating operating models that can respond effectively when unexpected events occur.

How to Build a Risk Management Program for Your Business

Building a risk management program does not require a large team or complex technology from day one. The most effective programs start with a clear understanding of business objectives, establish consistent processes, and gradually mature over time as risks and organizational needs evolve.

The following 6 steps provide a practical roadmap for creating a risk management program that supports business resilience, regulatory compliance, and long-term growth.

1. Define Risk Appetite and Tolerance

The first step is determining how much risk the organization is willing to accept in pursuit of its objectives. Some risks may be acceptable if they support growth and innovation, while others may require immediate action due to their potential impact.

Establishing a clear risk appetite helps leadership make consistent decisions and guides prioritizing risk management efforts across the organization.

2. Identify and Categorize Risks

Once risk appetite is defined, organizations should identify the risks that could affect their operations, finances, reputation, compliance obligations, and strategic objectives. This process should involve stakeholders from different departments to ensure a complete view of potential exposures.

Grouping risks into categories such as strategic, operational, financial, cybersecurity, and compliance risk makes them easier to assess and manage.

3. Build a Risk Register

A risk register is a central document used to record identified risks, their potential impact, likelihood, ownership, and planned response actions. It provides a single source of truth for tracking risk information across the organization.

Maintaining an up-to-date risk register improves visibility, accountability, and communication between business units and leadership teams.

4. Select a Risk Management Framework

A framework provides the structure and guidance needed to manage risks consistently. Organizations should select a framework that aligns with their industry, regulatory requirements, and business objectives.

For example, ISO 31000 provides broad risk management principles, NIST RMF focuses on cybersecurity risk, and COSO ERM integrates risk management into governance and strategic planning.

Read more: Enterprise Risk Management (ERM): Framework, Software & Implementation Guide

5. Assign Ownership and Establish Governance

Risk management works best when responsibilities are clearly defined. Each significant risk should have an owner responsible for monitoring, reporting, and coordinating mitigation activities.

Organizations should also establish governance mechanisms, such as risk committees, executive oversight, and regular reporting processes, to ensure that leadership maintains visibility into key risks and emerging issues.

6. Monitor, Review, and Improve

Risk management is a continuous process rather than a one-time project. Risks change as business priorities evolve, regulations are updated, technologies advance, and new threats emerge.

Regular reviews help organizations evaluate the effectiveness of controls, update risk assessments, and identify emerging risks. As programs mature, many organizations adopt risk management or GRC platforms to automate monitoring, reporting, and risk tracking activities.

Conclusion

Risk management is no longer just about avoiding losses or satisfying compliance requirements. In today’s business environment, it has become a strategic capability that helps organizations make better decisions, respond to uncertainty, and build long-term resilience.

Whether the risk involves cybersecurity threats, operational disruptions, regulatory change, financial uncertainty, or emerging technologies, the goal remains the same: understand potential impacts before they become business problems and take appropriate action to manage them. Organizations that embed risk management into daily operations and decision-making are better positioned to protect their assets, maintain stakeholder trust, and pursue growth with confidence.

As risk landscapes continue to evolve, successful organizations will move beyond periodic assessments and reactive controls toward continuous monitoring, stronger governance, and more resilient operating models.

If your organization is looking to strengthen its risk management capabilities, consulting with Terralogic can help you establish governance structures, implement proven frameworks, and build a more proactive approach to managing business risk.

FAQs

1. What is risk management in simple terms?

Risk management is the process of identifying, assessing, and controlling events that could affect an organization’s objectives. It helps businesses understand potential threats, evaluate their impact, and decide whether to avoid, reduce, transfer, or accept specific risks. The goal is to minimize disruption while supporting informed decision-making and sustainable growth.

2. What are the 5 steps of the risk management process?

The 5 steps of the risk management process are:

- Risk Identification – Identifying potential risks that could affect business objectives.

- Risk Assessment – Evaluating the likelihood and potential impact of each risk.

- Risk Prioritization – Ranking risks based on severity and business impact.

- Risk Response – Deciding whether to avoid, reduce, transfer, or accept the risk.

- Monitor & Review – Continuously tracking risks and updating mitigation plans as conditions change.

3. What are the main types of risk in business?

The most common types of business risk include:

- Strategic Risk – Risks related to business decisions and long-term objectives.

- Operational Risk – Risks arising from people, processes, systems, or day-to-day operations.

- Financial Risk – Risks that affect revenue, profitability, cash flow, or financial stability.

- Compliance Risk – Risks associated with legal, regulatory, or industry requirements.

- Reputational Risk – Risks that could damage public perception or stakeholder trust.

- Cybersecurity Risk – Risks involving data breaches, cyberattacks, or technology failures.

- ESG & Climate Risk – Risks related to environmental, social, and governance factors.

4. What is the difference between risk management and enterprise risk management (ERM)?

Risk management can refer to managing risks within a specific department, project, or business function. The focus is often limited to a particular area of responsibility.

Enterprise Risk Management (ERM) takes a broader, organization-wide approach. It evaluates strategic, operational, financial, cybersecurity, compliance, and other risks within a connected portfolio. ERM integrates risk considerations into governance, planning, and executive decision-making, helping leadership understand how different risks interact across the business.

Keep reading about

LEAVE A COMMENT

We really appreciate your interest in our ideas. Feel free to share anything that comes to your mind.

Let's Craft Brilliance

Just exploring? Let's think out loud together. We would love to hear from you. Come, let's get started!